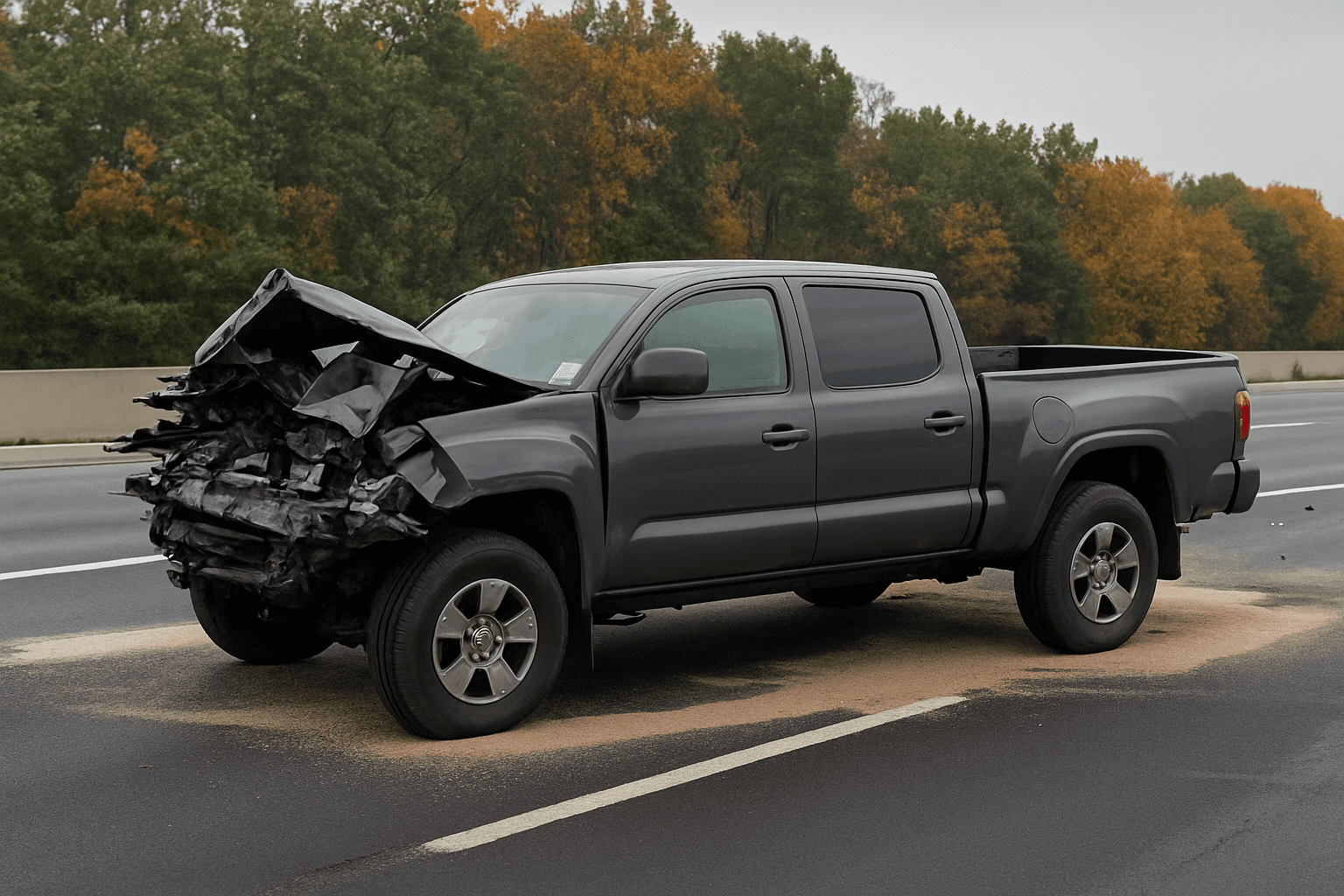

Leaving the scene triggers felony-level underwriting in most states. Non-owner SR-22 carriers treat hit-and-run differently than DUI — some won't write the policy at all, and those that do price it 40-80% higher than standard non-owner SR-22.

Why Leaving the Scene Changes Non-Owner SR-22 Underwriting Entirely

Leaving the scene of an accident — even a minor property-damage crash — is classified as a felony-level violation in most states' underwriting databases. Non-owner SR-22 carriers see it differently than DUI, reckless driving, or uninsured motorist suspensions. The distinction matters because non-owner SR-22 is already a specialty product with a limited carrier pool, and hit-and-run violations eliminate roughly half the carriers who would otherwise write non-owner policies.

The trigger is the reporting code your state DMV assigns to the violation. Most states classify leaving the scene as a "moral hazard" violation — a category that includes insurance fraud, theft, and intentional harm. DUI is a high-risk category, but it's predictable. Carriers have decades of actuarial data on DUI recidivism and claim frequency. Hit-and-run has no such predictability, and underwriters treat unpredictable risk as uninsurable risk.

If you sold your vehicle after the suspension or never owned one to begin with, non-owner SR-22 is still the correct product. The challenge is finding a carrier willing to file. The hit-and-run code in your driving record triggers automatic declines at most standard carriers and many non-standard carriers. The carriers who remain price the policy as though you present both high accident frequency AND high claim-evasion risk. That combination produces premium increases of 40-80% over standard non-owner SR-22 rates.

Which Non-Owner SR-22 Carriers Write Hit-and-Run Cases

Progressive and Acceptance Insurance write the majority of non-owner SR-22 policies for hit-and-run violations nationally. Bristol West and Dairyland write selectively in states where they have appointed high-risk divisions. The National General and Foremost write in fewer than 20 states and require manual underwriting review for any felony-level violation.

The carrier pool shrinks further if your state requires FR-44 filing instead of SR-22. Florida and Virginia mandate FR-44 for DUI-related suspensions, but leaving the scene falls outside that trigger in most cases unless alcohol or drugs were involved. If your suspension letter specifies FR-44, the non-owner carrier pool drops to Progressive, Dairyland, and occasionally Bristol West. Most FR-44-capable carriers won't write non-owner policies for hit-and-run violations at all.

Expect multiple quote declines. Aggregator tools auto-decline hit-and-run codes at the first screen because their carrier contracts prohibit binding those risks online. You'll need to call non-standard SR-22 specialists directly. When you do, ask whether the carrier underwrites non-owner SR-22 for "leaving the scene" violations specifically — not just "SR-22" generically. The difference determines whether you spend 20 minutes or two weeks finding coverage.

Compare car insurance rates in your state

Get quotes from licensed carriers — no obligation, no spam, results in minutes.

Get Your Free Quote✓ No Obligation Required✓ Licensed Carriers Only✓ Available Nationwide✓ Free to Compare

How Much Non-Owner SR-22 Costs After Leaving the Scene

Non-owner SR-22 for a clean-record driver costs $25-$50/month in most states. Add a standard DUI, and that jumps to $60-$90/month. Add a hit-and-run violation, and expect $85-$160/month depending on state and carrier. The increase reflects felony-level underwriting and the reduced carrier pool.

The filing fee is separate from the premium. Most carriers charge $25-$50 to file Form SR-22 with your state DMV. That's a one-time charge at policy inception, not a monthly cost. If your state requires 3-year SR-22 filing and you let the policy lapse at month 18, the carrier files a cancellation notice with the DMV, your license suspends again, and you pay the filing fee a second time when you reinstate.

Florida and Virginia non-owner FR-44 costs more because the liability minimums are doubled. Standard SR-22 requires state-minimum liability limits — typically 25/50/25 in most states. FR-44 requires 100/300/50 in Florida and 50/100/40 in Virginia. Higher limits mean higher premiums. Expect $120-$200/month for non-owner FR-44 after a hit-and-run violation in those states. Estimates based on available industry data; individual rates vary by driving history, age, county, and carrier.

What Non-Owner SR-22 Covers When You're Reinstated

Non-owner SR-22 provides liability coverage when you drive a vehicle you do not own. That includes borrowed cars, rental cars, employer vehicles driven with permission, and family member vehicles you're listed as an occasional driver on. The policy pays for damage you cause to other people and their property — bodily injury liability and property damage liability only.

It does not cover the vehicle you're driving. There's no comprehensive coverage, no collision coverage, and no medical payments coverage for your own injuries. If you borrow a friend's car and crash it, your non-owner policy pays for the other driver's vehicle and medical bills. Your friend's collision coverage pays for their own car. If your friend has no collision coverage, their car stays damaged.

Non-owner SR-22 also does not cover any vehicle you own, lease, or have regular access to. If you acquire a vehicle during the SR-22 filing period — whether you buy it, receive it as a gift, or move in with someone whose car you'll drive regularly — you must convert to an owner SR-22 policy within 30 days in most states. Failure to do so can result in license re-suspension even if the non-owner policy stays active. The state DMV considers uninsured vehicle ownership a separate violation from uninsured driving.

How Leaving the Scene Affects SR-22 Filing Duration

SR-22 filing duration is set by state law and the violation that triggered the suspension, not by the carrier. Most states require 3-year SR-22 filing for hit-and-run violations classified as felonies. Some states impose 5-year filing if the leaving-the-scene charge involved injury or significant property damage. A few states reduce the filing period to 1-2 years if the charge was reduced to a misdemeanor through plea agreement.

The filing clock starts the day your SR-22 policy becomes active and the carrier files Form SR-22 with the state DMV, not the day of the violation or the day of conviction. If your suspension order was issued in January, you secure a non-owner SR-22 policy in March, the carrier files in March, and your state requires 3-year filing, your SR-22 obligation ends in March three years later. The suspension itself may end sooner — many states lift the suspension 30-90 days after SR-22 filing if all other reinstatement requirements are met — but the filing requirement continues for the full statutory period.

If your policy lapses for any reason during the filing period, the carrier files a cancellation notice with the DMV. Most states suspend your license again within 10-30 days of receiving that notice. You'll pay reinstatement fees a second time, and the SR-22 filing clock does not pause. Some states restart the full 3-year period from the date of the new filing. Verify current requirements with your state DMV before assuming the filing period resumes where it left off.

What Happens If You Get a Vehicle During the Filing Period

Non-owner SR-22 stops being valid coverage the moment you acquire a vehicle. Acquire means purchase, lease, receive as a gift, or gain regular access to a household vehicle. If you move in with a partner whose car you'll drive more than occasionally, most states consider that regular access.

You have two options: convert the non-owner policy to an owner policy with the same carrier, or buy a separate owner SR-22 policy and cancel the non-owner policy. Converting is usually cheaper and faster because the carrier already has your underwriting file and SR-22 is already on file with the state. The carrier adds the vehicle to the policy, adds comprehensive and collision if you want it, recalculates the premium, and continues the SR-22 filing without interruption.

If you don't notify the carrier and the state discovers you own an uninsured vehicle, the DMV will suspend your license again even if your non-owner SR-22 policy is active and paid. The non-owner policy does not extend to vehicles you own. The state views uninsured vehicle ownership as a separate compliance failure. Most states discover the gap when you register the vehicle, renew your license, or get pulled over and the officer runs your plates.

FR-44 Substitution in Florida and Virginia

Florida requires FR-44 filing instead of SR-22 for DUI-related offenses, but leaving the scene typically triggers standard SR-22 unless drugs or alcohol were involved in the underlying incident. Virginia requires FR-44 for DUI and certain aggravated reckless driving cases. If your suspension letter specifies FR-44, you cannot substitute SR-22. The filing codes are different, and the DMV will not lift your suspension if you file the wrong form.

Non-owner FR-44 carriers in Florida include Progressive, Bristol West, and Dairyland. In Virginia, Progressive and Acceptance write most non-owner FR-44 policies. Premiums are higher than non-owner SR-22 because FR-44 requires 100/300/50 liability limits in Florida and 50/100/40 in Virginia, compared to 10/20/10 minimums for standard SR-22 in most states. Expect to pay $120-$220/month for non-owner FR-44 after a hit-and-run violation in those states.

The FR-44 filing fee is separate from the premium and typically runs $50-$75 at policy inception. If the policy lapses, the carrier files a cancellation notice with the Florida DHSMV or Virginia DMV, your license suspends again, and you pay the filing fee a second time when you reinstate. FR-44 filing periods in Florida and Virginia are typically 3 years from the date of filing, not the date of the offense.